Commentary

Corn moved higher on two fronts today in my opinion. First, national corn ratings now stand one point below last year and 8% behind the five-year average at 51% good to excellent. Top five producers Minnesota and Iowa held up those ratings with a two-point gain each this week, but both are holding safely on the low side of comparables heading into harvest. Only Ohio, North Dakota, and Indiana remain above their respective five-year averages with Michigan only a tick below.

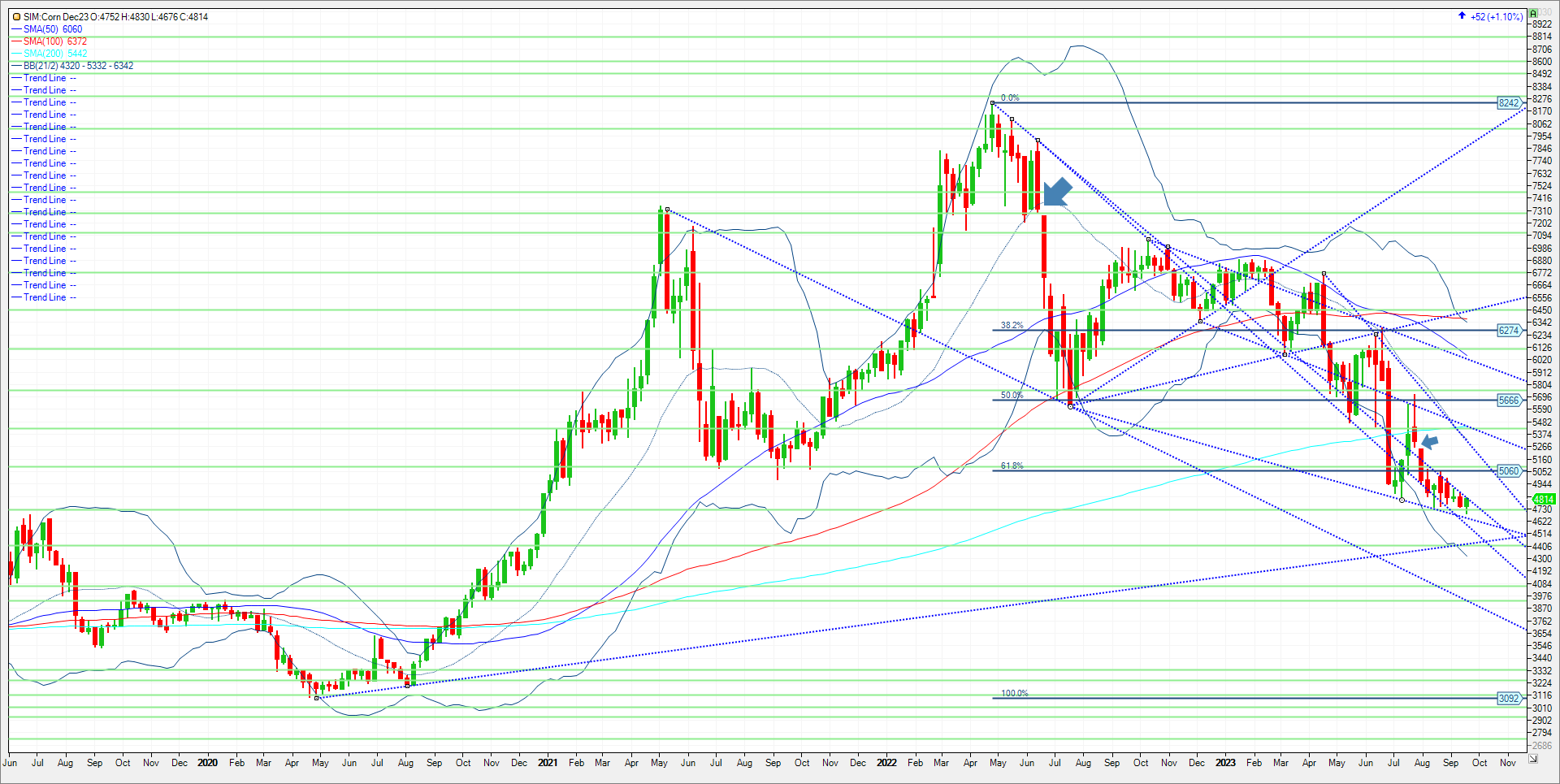

Second, Brazilian government supply agency CONAB sees 2023/24 total grain production at 319.5 million metric tons (MMT), down from 322.75 MMT in 2022/23; soybeans were pegged at 162.4 MMT, up from 154.6 MMT this past season, with acreage up from 44.1 to 45.3 million hectares (109.0 to 111.9 million acres). Total corn output was pegged at 119.8 MMT, down from 131.9 MMT in ‘22/23, with plantings there down from 22.3 to 21.2 million hectares (55.1 to 52.4 million acres). So, in my estimation the algos read the headlines, short covering was featured as managed money is short 135K contracts and we had the Fed talking today. Technically the market closed right at key resistance at 4.82. (See weekly continuous chart below).

The bearish argument for a sustainable corn rally is demand or lack thereof. China has been completely out the market so far for large scale US origin. USDA in their last WASDE is at a massive 2.2-billion-bushel corn carryout. That is approximately 750 million bushels above last year. We have another round of export sales tomorrow and perhaps that will be a reminder of the reality that we will have too much of everything soon as corn harvest advances. Second, while Brazil maybe planting less this year, Argentina could more than make up for any Brazilian shortfall. As the global climate has flipped from La Nina to El Nino, it has meant in previous EL Nino’s that Argentina gets cooler and wetter. More conducive for a sizable crop.

As always until we get some data points from USDA in the next three weeks, we will keep our opinions to a minimum and trade the charts. Resistance this week is at 4.82. We settled there today. There is not much in the way of resistance above 4.82 until 5.06/07 in my view. So, a strong close over could take the market there. However, that trendline moves down to 4.78 next week. Should we hold that level we could see an enhanced short covering rally. If the market can’t take out resistance, I see the market trading back down to 4.74 (30% down for the year threshold), and then major support at 4.63. A close below 4.63 and its 4.54 and 4.43 the next levels of support in my opinion.

Trade Ideas

Futures-N/A

Options-N/A

Risk/Reward

Futures-N/A

Options-N/A

Please join me for a free grain and livestock webinar at 3pm Central. We discuss supply, demand, weather, and the charts. Sign Up Now

Walsh Trading, Inc. is registered as a Guaranteed Introducing Broker with the Commodity Futures Trading Commission and an NFA Member.

Futures and options trading involves substantial risk and is not suitable for all investors. Therefore, individuals should carefully consider their financial condition in deciding whether to trade. Option traders should be aware that the exercise of a long option will result in a futures position. The valuation of futures and options may fluctuate, and as a result, clients may lose more than their original investment. The information contained on this site is the opinion of the writer or was obtained from sources cited within the commentary. The impact on market prices due to seasonal or market cycles and current news events may already be reflected in market prices. PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

All information, communications, publications, and reports, including this specific material, used and distributed by Walsh Trading, Inc. (“WTI”) shall not be construed as a solicitation for entering into a derivatives transaction. WTI does not distribute research reports, employ research analysts, or maintain a research department as defined in CFTC Regulation 1.71.