Commentary

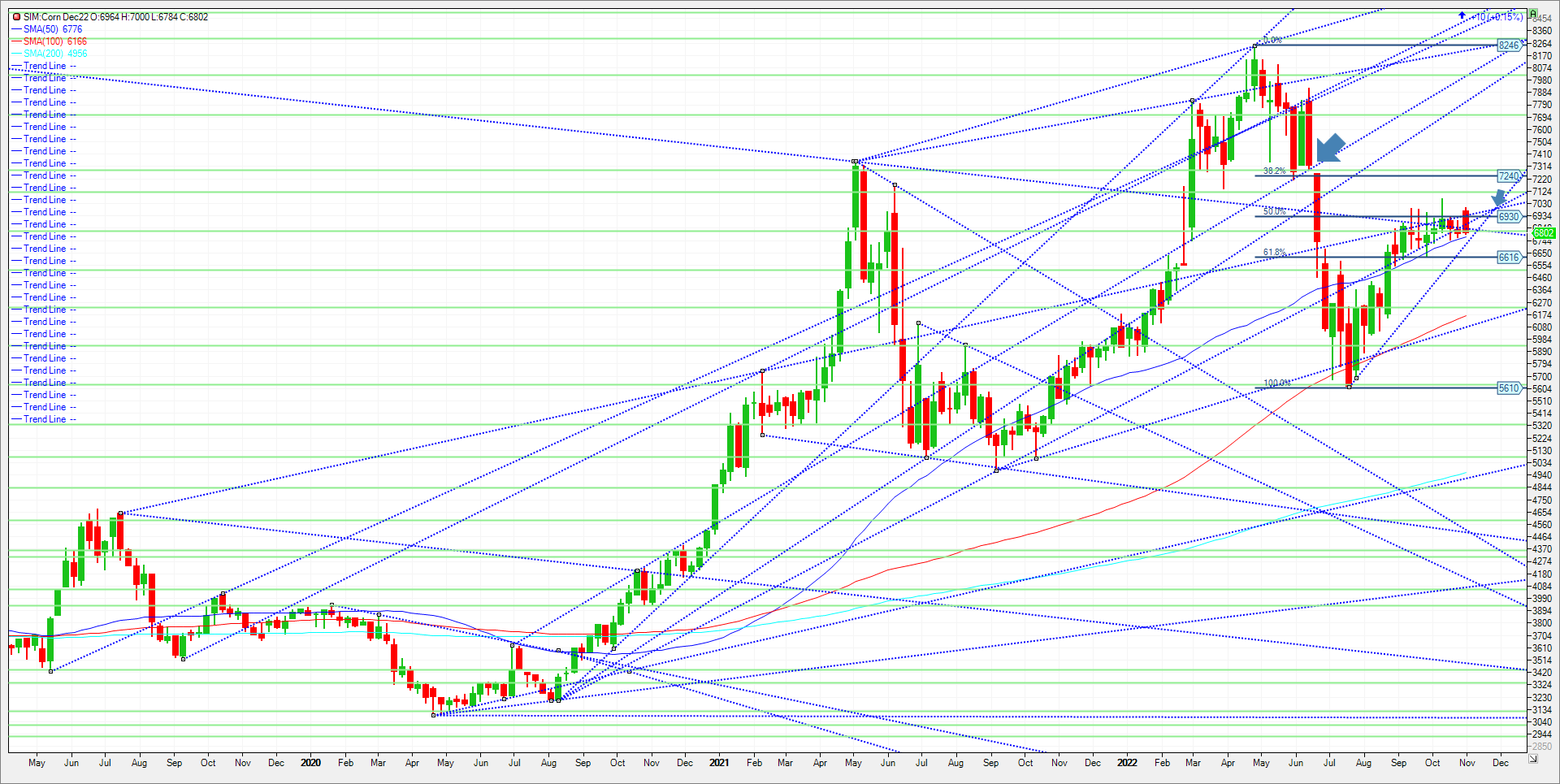

The Corn market’s sideways trade since mid-September may persist for a little while longer, with USDA’s Nov. 9 reports looming as the next price influencer in my opinion. Demand fundamentals have grown shakier, with the strong U.S. dollar, exports lagging, and Brazil corn exporters winning Chinese customs approval. In my view it could eat into U.S. demand. Export sales were a paltry 370K metric tons this week which is one-quarter of the volume contracted a year ago. This puts marketing year commitments at 14.5 million metric tons vs 31 million metric tons last year. The USDA demand forecast at present has sales for future shipment of US corn at 5 million metric tons smaller than the year prior, not the 16.5 million metric tons that currently sits on the books.

Unless buyers like China and Japan become much more aggressive, a near-term push above $7.00 maybe be difficult to achieve in my view. A tight supply outlook has limited price downside for the last two months as the 22/23 crop kept getting revised smaller in yield, however that could get revised on the 9th. Traders are looking for a yield of 171.9 BPA in Wednesday’s report, the same as last month. The range of guesses is from 171.0 on the low to 174.9 at the high. Ending stocks look to come in at 1.207 billion bushels vs 1.172 last month. The range is from 1.050 to 1.390 billion. Should we come in near the guesses without any surprises, I think corn is going to need help from wheat or beans to sustain a November rally. It is my belief that a long-term Corn rally will likely take a bullish catalyst, such as a weather threat to South America’s crop, to drive a strong, sustained rally. Uncertainty over the Ukraine export deal remains a major outside risk as the trend and index following funds have been reluctant to liquidate given the unknown of the grain export deal. Managed funds are long over 270K contracts. They may get uneasy down the road carrying a sizable long with a lack of demand. Traditionally we flip from a supply side to a demand driven market after the November WASDE. Some forecast models suggest that we will see a transition away from La Nina this winter, with some chance of moving toward El Nino by next growing season. That may suggest a shift toward a wetter weather pattern for the Midwest by Spring if it occurs, and better moisture chances in South America particularly drought-stricken Argentina. That said a lot could happen between now and then to change that. Technical levels for December Corn come in as follows. Major support is at 6.77/78 next week. A close under and the market could test 661 and then 6.52. Major resistance is at 6.95. A close above 6.95 is needed to test 7.12 and then the gap at 7.28.

Trade Ideas

Futures-N/A

Options-N/A

Risk/Reward

Futures-N/A

Options-N/A

Please join me for a free grain and livestock webinar every Thursday at 3pm Central. We discuss supply, demand, weather, and the charts. Sign Up Now

Walsh Trading, Inc. is registered as a Guaranteed Introducing Broker with the Commodity Futures Trading Commission and an NFA Member.

Futures and options trading involves substantial risk and is not suitable for all investors. Therefore, individuals should carefully consider their financial condition in deciding whether to trade. Option traders should be aware that the exercise of a long option will result in a futures position. The valuation of futures and options may fluctuate, and as a result, clients may lose more than their original investment. The information contained on this site is the opinion of the writer or was obtained from sources cited within the commentary. The impact on market prices due to seasonal or market cycles and current news events may already be reflected in market prices. PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

All information, communications, publications, and reports, including this specific material, used and distributed by Walsh Trading, Inc. (“WTI”) shall not be construed as a solicitation for entering into a derivatives transaction. WTI does not distribute research reports, employ research analysts, or maintain a research department as defined in CFTC Regulation 1.71.

Sean Lusk

Vice President Commercial Hedging Division

Walsh Trading

312 957 8103

888 391 7894 toll free

312 256 0109 fax

Walsh Trading

53 W Jackson Suite 750

Chicago, Il 60604