Commentary:

Increased demand most notably from China has driven the soy complex bid while minor dips in Corn remain buying opportunities. A falling US Dollar has stoked some inflation here in the grain and livestock sectors in my view as soymeal, wheat, and hogs have seen decent bounces. I think this continues in some shape or fashion into year end and early next year amid the uncertainties of the US Presidential election and key Congressional races. Then we have vaccine possibilities and the potential to get past the pandemic. I have previously written that trend and index following funds may look at commodity sectors that were downgraded and decimated by the pandemic particularly in the 2nd fiscal quarter, that may seem as inflatonary type bets as the Fed has printed an unprecendented 10 trillion dollars. It is my belief that their mandate now is to stoke inflation by keeping rates low into 2022 if economic conditions warrant. This reminds me of their actions in late 2008/09 to avert a financial meltdown following the housing crash. The circumstances while different this time due to the cause, could and should have perhaps the same type of inflationary response into 2021 and 2022. Again my opinion here but look at grain and livestock pricing in 2010 and 2011 from the deflationary lows of late 2008 and 2009. I see opportunity.

The Derecho that hit the Midwest in early August was another Black Swan entering in the market, this time bullish for grains in my view. It rattled Iowa, as 200 to 400 million bushels of corn could be lost. It created an unknown for the balance sheet and sent sizable funds that were short, scrambling to cover, while igniting physical demand from China. This week alone the Chinese have bought approximately 85 million corn bushels for future shipment. This morning China bought more beans (318K metric tons), while the Phillipines bought 175K metric tons of soymeal. China has been an active aggressive buyer of corn, beans, wheat, and pork as their reserves have been depleted amid lower domestic production in my opinion.

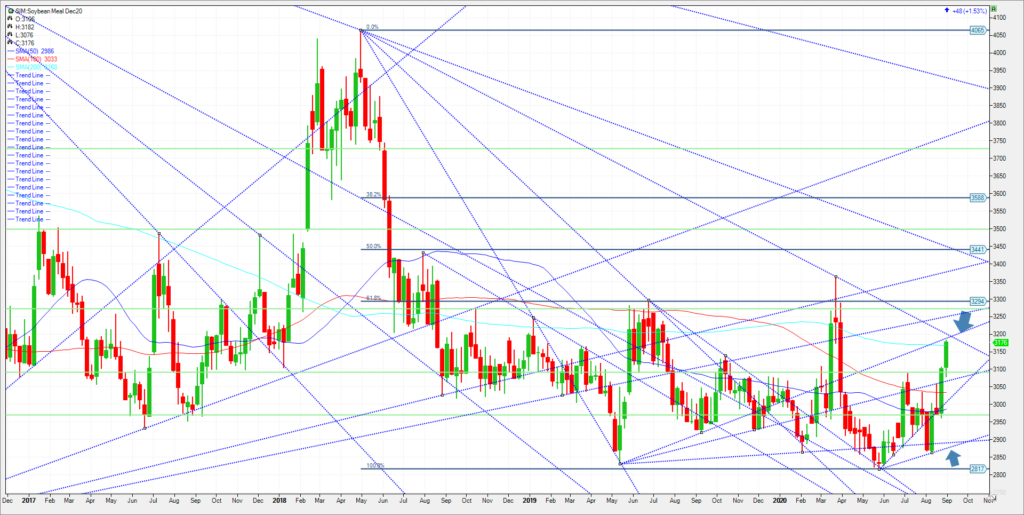

Weather can still impact future yields at home moving forward. Traders should monitor a potential frost/freeze event in the Midwest next week although confidence is low. A longer term LaNina that plays havoc with the Southern Hemisphere, which translates to hot and dry and drought like conditions needs to be watched longer term. Argentina is slashing yeild outlooks for winter wheatr and its starting to turn dry again in Australia. Included below is a weekly soymeal chart. We traded up to the 200 Day moving average basis Deccember Meal and the market looks poised over time to potentially make a run to the 50 percent retracement of 344. Big crop report next week on the 11th. We could see some consolidation into the report. Should we see the meal market pull back, I would be a buyer. Chart and trade idea below.

Trade Idea:

Futures-N/A

Options-Buy the March 2021 350/400 call spread. Work to buy on a bid of 3.50. That spread closed today at 4.70

Risk/Reward

Futures-N/A

Options-The risk if filled at 3.50 is $350.00 plus commissions and fees.Tight bet here and low risk. The maximum one could collect is 5K at option expiration, if we settle above 4.00 in late February at option expiration. In my view I would offer the spread at 20 points to collect 2K on the exit minus trade costs and fees.

Please join me each and every Thursday for a free grain and livestock webinar. We discuss supply, demand, weather and the charts.Sign Up Now

Walsh Trading, Inc. is registered as a Guaranteed Introducing Broker with the Commodity Futures Trading Commission and an NFA Member.

Futures and options trading involve substantial risk and is not suitable for all investors. Therefore, individuals should carefully consider their financial condition in deciding whether to trade. Option traders should be aware that the exercise of a long option will result in a futures position. The valuation of futures and options may fluctuate, and as a result, clients may lose more than their original investment. The information contained on this site is the opinion of the writer or was obtained from sources cited within the commentary. The impact on market prices due to seasonal or market cycles and current news events may already be reflected in market prices. PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

All information, communications, publications, and reports, including this specific material, used and distributed by Walsh Trading, Inc. (“WTI”) shall be construed as a solicitation for entering into a derivatives transaction. WTI does not distribute research reports, employ research analysts, or maintain a research department as defined in CFTC Regulation 1.71.