Commentary:

Grain prices faced some headwinds to begin the week as renewed virus concerns emerged over the weekend in Europe. Stock Indices plunged Sunday Night into Monday taking grain and energy prices with them albeit for a short time in the grain complex. By the close yesterday, we were in the green on the grain board, as funds and specs buy dips amid defending their sizable long position in the market in my opinion. Virus fears are always going to be a headwind into 2021. Until global populaces can get access to the vaccine with no major side effects, headwinds will exist. But now we have a growing list of countries that are instituting grain export quotas or taxes to deter producer selling abroad. We had Russia last week with wheat, and then beans. Now we have China selling out of their reserves again with Corn which is an oddity for this time of year there. China sold all 103,455 MT of corn at an average price of 2,491 yuan/MT from the state reserve auctions. Heilongjiang will offer around 1 MMT of corn on Thursday. China also sold 59,201 MT of 2019 imported soybeans from its reserves. Also reported today was the Malaysia export tax for January crude palm oil is 8%, which is the maximum tax rate. This rate kicks in when prices are above 3,450 ringgit/MT. Export duties start at 3% when FOB prices are between 2,250-2,400 ringgit/MT. The optics on these measures initiated by governments across the globe are not bearish in my view, they add up as smaller bits of bullish fundamental news entering into the market. You couple that with weather hiccups in major producing areas, and the result is what you see now with 12.50 beans, 4.40 corn and plus 6.00 Chicago wheat. In my view, the effects of the pandemic of increased food consumption amid a short crop in some places have caused some food inflation. This isn’t going away until Spring and Summer harvests occur in the Southern Hemisphere and for winter wheat in the North.

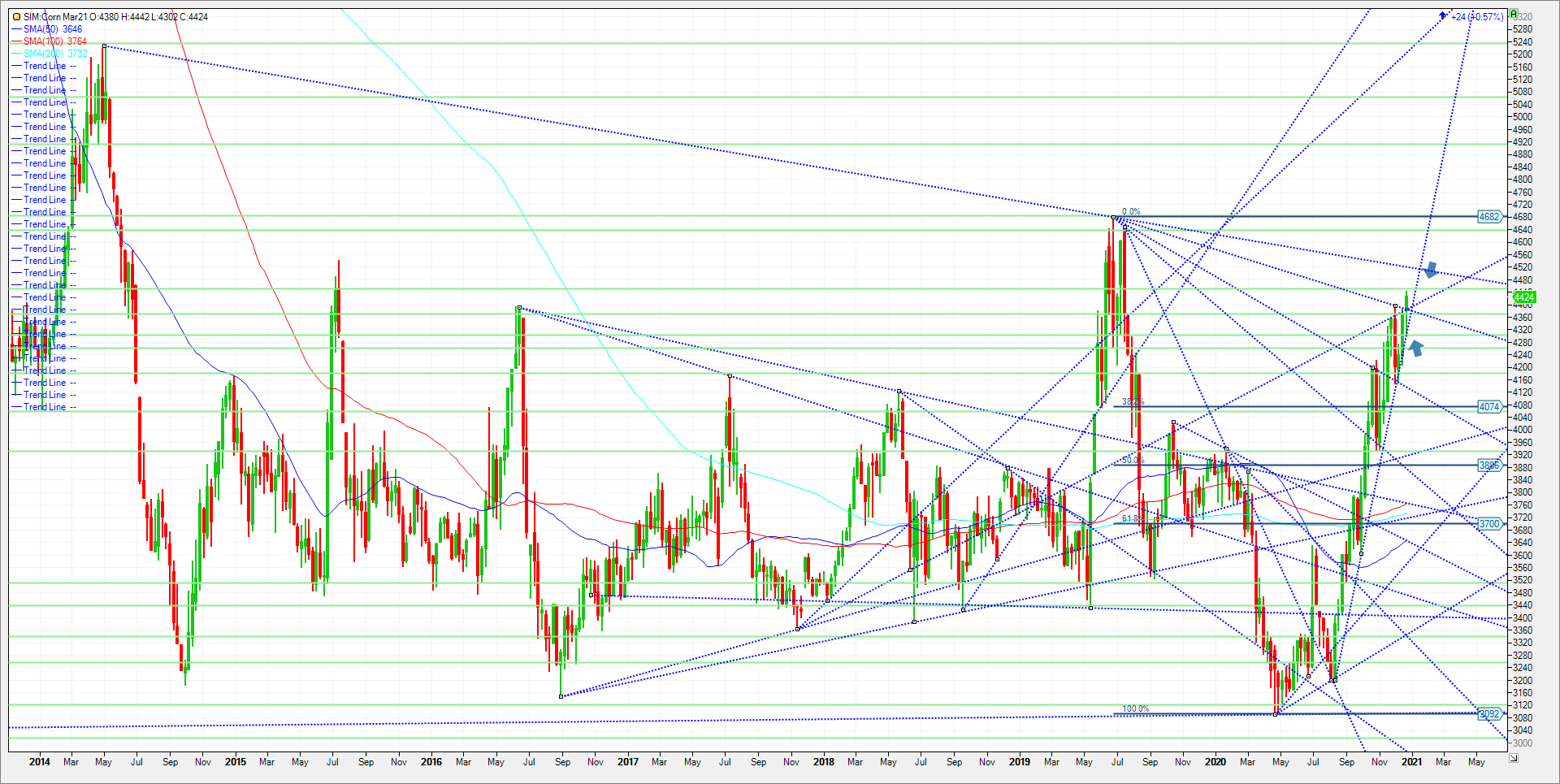

Make no mistake, producers holding onto crops around the globe looking to sell at the top will eventually sell. After all it is a weather market, and with forecasts likely shifting in the months to come, its simply a timing event at this point. We have a major crop report on the Jan 12th. We have month and quarter and year end coming too. Funds are long approximately 800K contracts across the grain complex. It’s a massive long in the market. Considering the low ending stocks for corn and wheat and especially beans, the long is warranted in my opinion. Brazil is the number one bean producer in the World. Weather forecasters in my view note that both southern and Center-South areas of Brazil are averaging very close to normal, to even slightly above normal precipitation for the month. Southern areas are seeing their wettest December since 2015. Yet, rainfall totals in the Center-West areas (Mato Grosso) are the third driest of the past four decades, while the Northeast is in its fourth driest December of the past 40 years. These latter two regions are expected to see some relief this week, but they trend drier again in the January outlook. This leaves 35 – 50% of the soybean belt at risk of yield reductions this year. With 65 percent of this year’s bean crop already booked for future shipment, the uptrend will remain intact unless a major shift in weather takes place in South America. In any event corn will follow beans in my view. Weakness in energy will not help corn as it relates to ethanol demand, and while future sales are robust, export shipments lag. Weekly corn chart included. Watch the trendline indicated by the upward arrow. 4.36 needs to hold in my view, a close under and I wouldn’t be long. We could see a push to support to 4.26 and then 4.14 and possibly all the way to 4.06/07. If support holds, I think the market eventually tests 4.52 and then 4.64. Call or email me with questions on trade ideas. 888 391 7894 or slusk@walshtrading.com

Trade Ideas

Futures-N/A

Options-N/A

Risk/Reward-N/A

Please join me for a year end webinar on New Year’s Eve at 1:30 pm. If you cannot attend live, a recording will be sent. We will discuss supply, demand, weather, and the charts as well as trade ideas. Sign Up Now

Walsh Trading, Inc. is registered as a Guaranteed Introducing Broker with the Commodity Futures Trading Commission and an NFA Member.

Futures and options trading involve substantial risk and is not suitable for all investors. Therefore, individuals should carefully consider their financial condition in deciding whether to trade. Option traders should be aware that the exercise of a long option will result in a futures position. The valuation of futures and options may fluctuate, and as a result, clients may lose more than their original investment. The information contained on this site is the opinion of the writer or was obtained from sources cited within the commentary. The impact on market prices due to seasonal or market cycles and current news events may already be reflected in market prices. PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE RESULTS.

All information, communications, publications, and reports, including this specific material, used and distributed by Walsh Trading, Inc. (“WTI”) shall be construed as a solicitation for entering into a derivatives transaction. WTI does not distribute research reports, employ research analysts, or maintain a research department as defined in CFTC Regulation 1.71